|

By Adam Schaub, Vice President of Platform Product Management, RegEd |

|---|

Construction

FPs are busy and want to focus on their clients, and compliance personnel are also tasked with a considerable amount of ongoing work. With these two factors in mind, consideration needs to be given to the number of questions as well as the volume that will require follow-up. You will want reps to be able to complete the ACQ in a reasonable time frame (approx. 30 minutes or less). For the volume of follow-up tasks, use 2% to 5% as a top-level guideline for the number of “incorrect” responses you can expect, and calculate the number of anticipated follow-up tasks based on your number of reps and the number of questions that will require follow-up.

You should try to keep questions the same or similar from year to year for continuity purposes and to look for trends. Of course, you will want to adjust any questions that have generated a lot of false positives. Also, when reviewing your questions, look to see if there are ones that apply to a branch level as opposed to an FP level. This may produce an opportunity for you to create a branch office annual questionnaire that would be distributed to branch managers or other appropriate persons to respond. This will reduce the number of ACQ questions and the amount of time spent on the ACQ for the FP base at large. Also, this prevents situations where one FP at a branch answers a question differently from another, as this will cause more follow-up on the back-end for everyone involved.

Use clear language and avoid jargon, and leverage the capabilities your ACQ platform has with regard to creating definitions, informational bubbles, and hover-over text. You don’t want the FP (or multiple FPs) to misunderstand the question.

If your ACQ platform allows you to integrate with your OBA or Outside Account solution as well, consider taking advantage of that so that FPs can take care of these outstanding issues all at the same time.

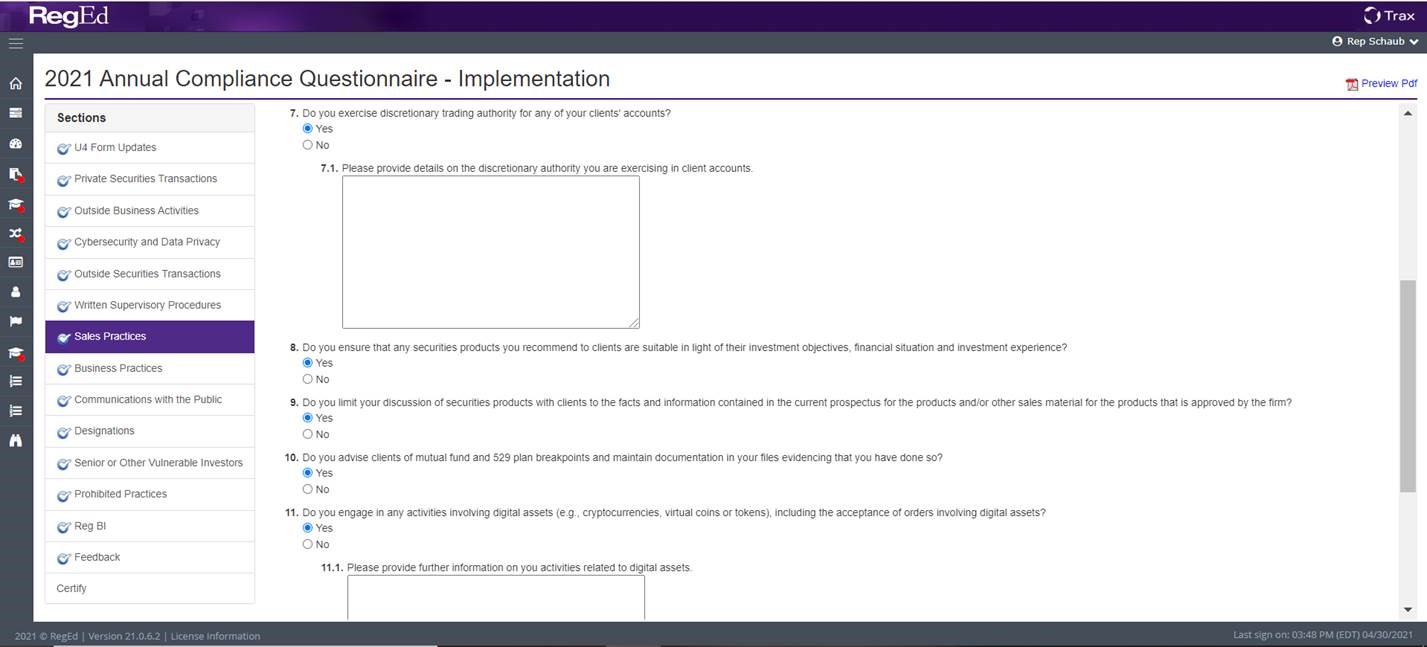

When writing questions, associate a question with a specific time period. For example, if you ask “have you ever engaged in a PST,” reps that did so and received approval or those that had to discuss this same PST with the Compliance team on last year’s ACQ will no doubt get annoyed that they must disclose the same thing each year. You can use time-frames such as “Since the last ACQ,” “During this calendar year,” or ‘In the past 3 years.”

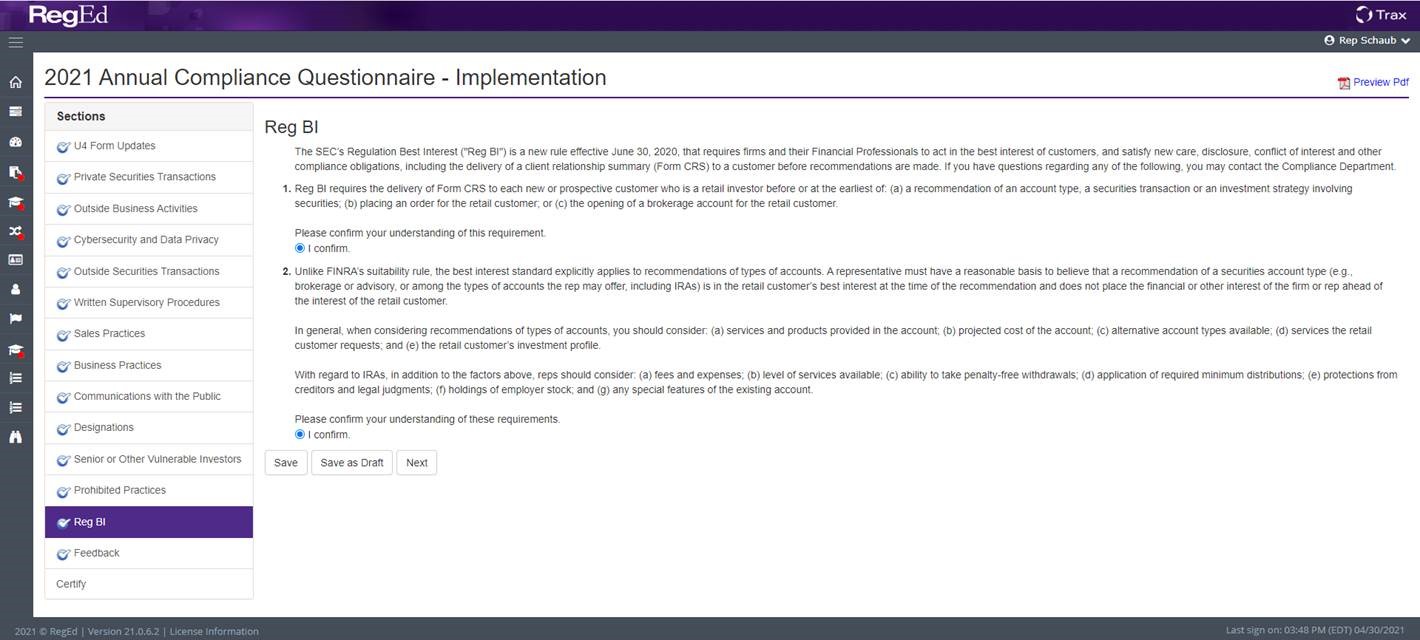

Rather than strictly using “yes” or “no” answer choices, consider having a single answer choice for the FPs to confirm their understanding. For example, if you pose a question such as “Are you aware that you should not act on trade instructions received via email? Answer Choice: Select Yes or No,” your firm will need to do follow up with all of the “No” responses. Instead, either have a branching question for the “No” response or reword the original question so that the FP has to confirm their understanding before proceeding. For example, construct the question as: “The firm’s policy prohibits FPs from acting on trade instructions received via email. Please confirm your understanding: Answer Choice: I Confirm”. The FP cannot move on until they’ve confirmed their understanding.

Having FPs confirm within the questionnaire is an easy way to demonstrate to FINRA that your FPs understand a specific policy, and it will save you time from having to follow-up and discuss it with the FP or provide them other training. However, you probably don’t want to take this approach with more serious issues, such as private securities transactions. If an FP doesn’t understand that engaging in a PST is problematic, you’ll want to set them on the right track directly.

Also, you may have read that you should flip between yes and no answers so that reps don’t just click yes all the way down. While this will make the FPs slow down and read each question (once they determine they can’t just mark each answer “yes”), weigh this benefit with the risk that you will have FPs that don’t catch on and who will mark a large number of incorrect answers for your compliance team to follow-up on.

As part of their responses, have your FPs provide details where needed; otherwise, you will need to follow up outside of the questionnaire or in a task. Doing follow-up just to get further details that you could have obtained within the questionnaire itself is an inefficient way to collect this information.

At the end of the ACQ, have FPs confirm their overall responses and attest their understanding of the consequences for providing incorrect information. Also, consider using a question at the end to get feedback on matters like the questionnaire, your CE program, or any areas in which the FP feels they need training.

Finally, include a catch-all question that allows FPs to provide any additional comments or context to any of their responses on the ACQ.